Imagine there are 2 people offering you a reward for letting them hold your money:

- Person A offers you 0.01%, but you know them.

- Person B person offers you 5%, but you’re not familiar with them.

After 1 year, $10,000 of your money earns $1, or $500 depending on who you pick.

This hypothetical explains why so many people skip out on earning more money with high yield savings accounts, and instead stick with banks that pay them almost zero interest.

It’s all about trust.

Before diving in, here’s a quick outline with jump links to each section:

- The game that banks play with your money

- The mind hack to get started with new bank accounts

- How much money should you transfer? The break-even technique

- Shopping for banks is like shopping for new grocery stores

- How to choose a good account + what I use

- Putting it all together

The game that banks play (with your money)

I worked on the launch of Credit Karma Money™ Save, so I know a thing or two about HYSAs—high yield savings accounts.

New fintech (“financial technology”) companies face the challenge that consumers either 1) don’t know about them and 2) don’t trust them yet.

So they have to offer something to attract customers away from the big banks…like higher interest rates.

People new to HYSAs wonder: how are these banks able to offer higher interest rates? Is this a scam?

This can be explained by the game that banks play:

- One way banks make money is by earning interest on the money you give them. (They can also offer loans and other banking service)

- Banks can earn the federal funds rate buying treasuries, which pays more than 5% right now

- Banks earn the difference between what they can earn (5%) and what they pay consumers (0.01%)

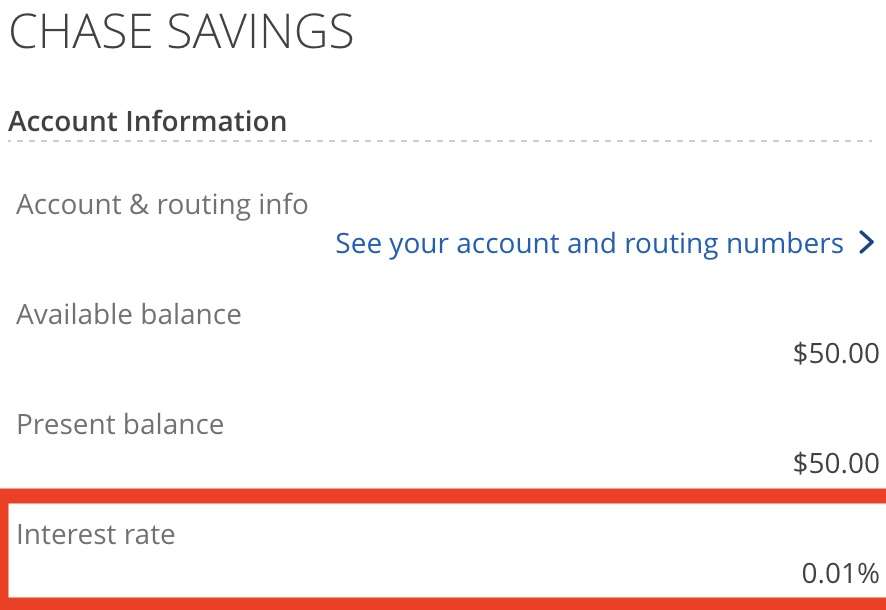

Because people are familiar with big banks like Chase, Wells Fargo, and Bank of America, those banks can afford to pay consumers waaaay lower interest. I have a “savings account” at Chase for research purposes, and they pay the same laughable amount as their checking account: 0.01%.

So these big banks are earning money hand over fist…because they can.

People’s relationships with banks are sticky. You might still be banking with that credit union down the street from your house. Or your Mom opened up a WaMu account for you, which then became a Chase account (OK, this is me). Conditioning runs deep.

So the prospect of moving banks can feel disproportionately big and emotional.

But it doesn’t have to be.

The mind hack to get started with new bank accounts

As a money coach, I never thought I’d have to to convince clients so hard to get free money by using high-yield savings. Friends, clients and family have tens of thousands of dollars in excess cash just sitting in accounts that could otherwise earn them hundreds a year.

After I tell them about earning free money, their interest is piqued…then months and years pass by.

Something occurred to me when I walked a client through the process of opening a new savings account. They said: “I’m scared of moving all my money over.”

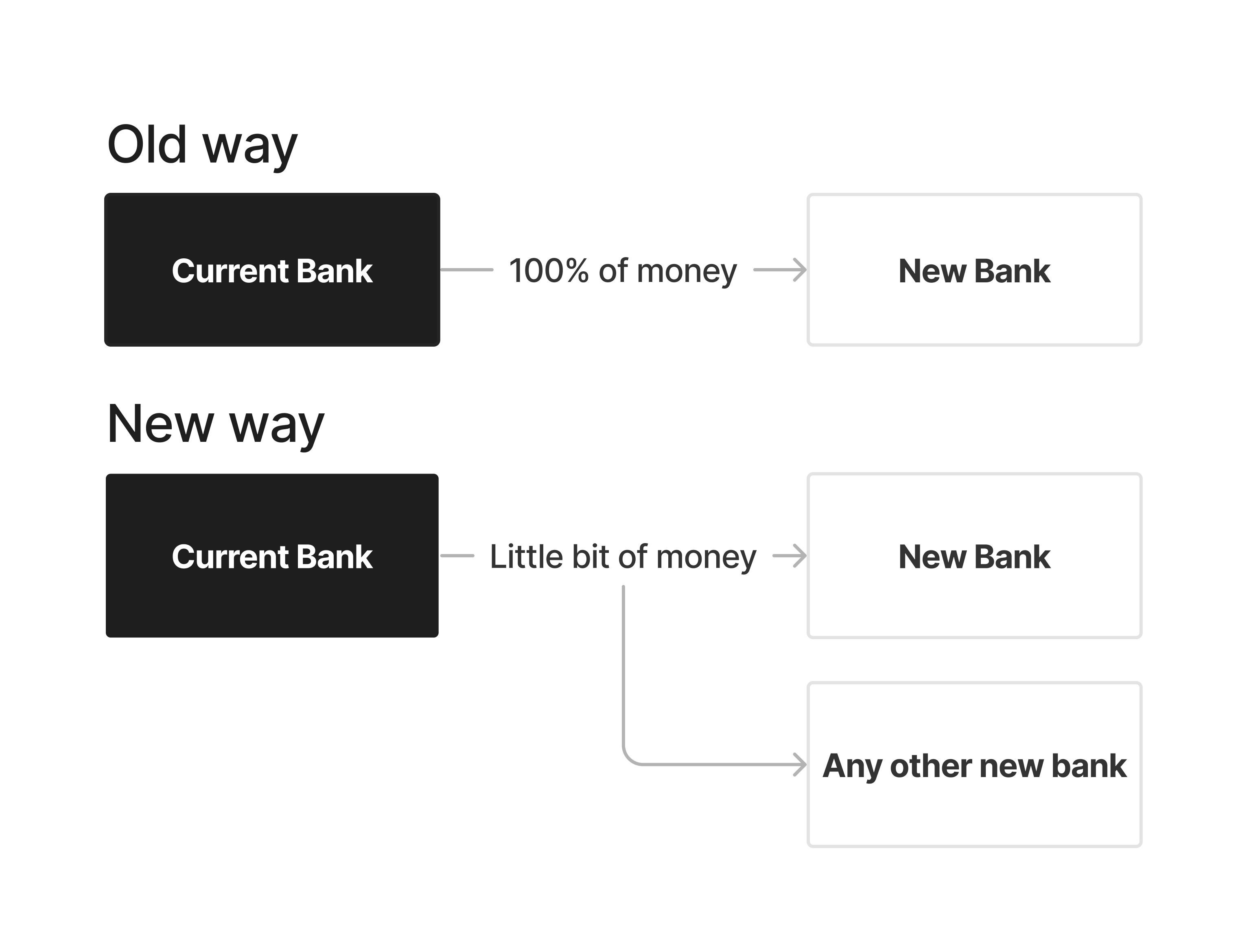

Aha! There’s a perceived “all or nothing” switching cost when it comes to opening new accounts.

The key to getting started is to transfer just a little, not a lot.

You do not need to be in a monogamous relationship with your current bank.

Modern technology makes linking bank accounts for transfers quite easy.

You can be promiscuous with your money and be a slut for interest.

How much money should you transfer? The break-even technique

Naturally, the next follow up question is: how much money should I put in there?

Find the break-even point at which you’ll be earning the same amount of interest, with less money.

Let’s say you have $10,000 available to transfer, and your current bank pays you 1%. The new bank you’re evaluating pays 5%.

Break even point = [Money in current account * Current interest rate] divided by New interest rate

So that would look like: ($10,000 * 1%) / 5% = $2000.

The break-even point amount is $2,000. Transferring $2,000 to the new 5% interest account will generate the same amount of interest as keeping the entire $10,000 in the old account paying 1% interest.

This way, you can reduce the perceived risk of moving all your money to the new account. Try it out, earn higher interest, and you can always transfer more over time.

Pro tip: after you figure out your monthly spending, you’ll see how much excess cash is left in your checking account. Consider transferring this excess to your high yield savings account.

Shopping for banks is like shopping for new grocery stores

The closest grocery store to me is a Food4Less, so I’ve shopped there for years.

I noticed the prices were often cheaper for the exact same product than if I had bought them at Ralphs.

Imagine my surprise when one day, I saw a Ralphs truck pull into the cargo bay of my local Food4Less.

(Turns out, Ralphs and Food4Less are owned by the same company—Kroger.)

Just as the same groceries can cost less literally from store to store, your dollars can earn different interest rates from bank to bank.

No one says you have to shop at Ralphs, Food4Less, or Aldi permanently.

But if you’re trying to get more for your dollar, it’s probably a good idea to check out discounted grocery stores once in a while. Maybe over time, you’ll see how much you’re saving and shop at new places more often. You might have to bag your own groceries though ;)

How to choose a good account + what I use

The top 4 factors I look for in any bank account: FDIC insurance, ease of use, no fees, and interest rates.

While I’ve rotated through a lot of savings accounts including Marcus and Discover bank, I keep going back to the Wealthfront Cash account, which I’ve had since 2019.

FDIC insurance: make sure your bank’s legit

If a bank is FDIC-insured, then the Federal Depositor Insurance Company will create a new bank to hold customer funds. While an unlikely scenario, the 2023 crash of Silicon Valley Bank demonstrates the real-life use case of FDIC insurance.

You can use the official BankFind tool to see if a bank is FDIC-insured.

Note: online neobanks are often backed by partner banks. For example you won’t find “Wealthfront” directly on the FDIC search website, because Wealthfront uses partner banks (which can be found on BankFind). This is what allows Wealthfront to provide $8 million FDIC coverage versus the standard $250,000.

Ease of use + solid features

If you’re going to be putting money in an online bank, then it better be easy to use.

I’m taking shots here, but I once put my money in CIT bank because they were paying some of the highest rates at the time. But this bank was nearly impossible to log in with a confusing security process. And this was confusing for me—someone who designed online bank accounts!

So a little higher interest isn’t worth a poor banking experience.

In comparison, Wealthfront is a dream to use:

- Slick user experience and app

- Fast transfers, including real time payments / same day withdrawals to eligible banks

- FDIC-insured up to $8 million

- Add money to different goals like “Vacation” and “Taxes” —it’s all held in the same account.

Wealthfront doesn’t just get the important basics right, but they’re innovators that continually add new features.

No fees + good business model

Any decent online bank should be free to use. That means no overdraft fees, no transfer fees, no minimum balance fees. Beyond no fees, I feel more confident putting my money with a bank that has a business model that allows them to make money.

You might have noticed that the account I use is called the Wealthfront Cash account, and it’s technically not a “high-yield savings” account. That’s because it could also be used as a checking account. You can get a debit card to spend your money, direct deposit to…or not, and just use it as a savings account that earns interest.

Having a diversified business model like checking and investing means that Wealthfront is trying to win over more of your dollars with value-added services. In contrast, I’m more wary of one-trick ponies that only offer a higher interest rate.

I don’t currently use Wealthfront’s investing products – which do charge a fee. I hold investments elsewhere. But if I decide to, there’s lower friction since I already have savings in Wealthfront. I respect the biz.

High interest with good features

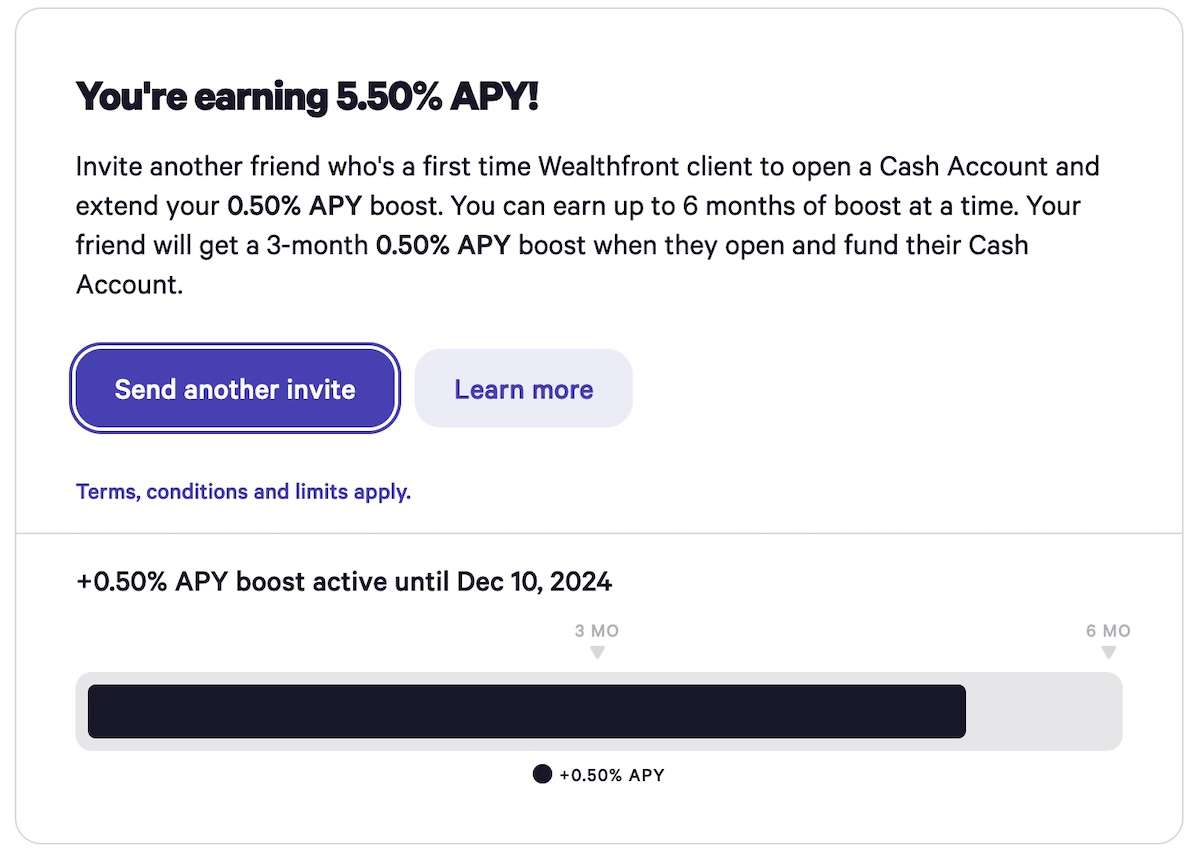

Of course, I wouldn’t be using Wealthfront if it didn’t have a competitive APY. It has one of the highest in the game at 5% currently.

By using my referral link, we both get a 0.5% APY boost to 5.50%. Once you get an account, you can also referral friends and get this boost for 3 months for every person you refer.

All those things being equal, I’m happy to move my money to a new higher-interest account as long as they meet these criteria.

(Remember, interest rates can change any time – across any bank).

Putting it all together

Let’s say you have an extra $10,000 in your checking or savings. And you’re sold on the idea of earning more interest for free. Here’s how to apply the ideas based on this article:

- Feel relief that you can be promiscuous with your money; you don’t have to transfer all your money or switch bank accounts

- Open a Wealthfront Cash account with a boosted APY from my referral link

- Transfer just a little bit of money to get comfortable

- Step it up and transfer the break-even amount of money that’ll make you the same amount of interest

- Become a fan and start referring your other friends to earn more interest

And if all else fails, I offer “over your shoulder” money coaching to help you implement new financial habits like this in real time so you don’t have to do it alone.

Thanks for your reading, and your interest ;)