Compliment of the week: You’re just the right type.

I’ll start off this newsletter with a rant about realizing the type of investor I am, then: Investor Amnesia, Solana, Evergrande, Lowest common denominator advice, and Cost of Living.

🤷🏽♂️ “That’s the type of investor you are”

There are many times when I think to myself: “If X stock goes down, then I’m definitely going to buy.”

In March 2020, the market took a massive hit. The investments I was interested in were at fire-sale prices. Did I hoard the companies and cryptos I believed in? No, I didn’t.

I thought through how I behaved as an investor, and uttered to myself: “That’s the type of investor you are.”

When you’ve identified the type of investor you are, there are 2 clear directions to try:

- Change yourself and hope to improve

- Adapt your investing style to fit how you are

There’s a lot of power in starting with #2. Change is hard; why not work with what you already have?

Personal examples:

- I’m not good at timing the market. Instead, I’ll use dollar cost averaging to buy into investments gradually and automatically

- I’m not good at picking specific investments. Instead, I invest in indexes, or things that represent broad trends I believe in.

- I tend to hold investments for a long time, and don’t often cut my losses. To fit this style, I’ll spend more time researching before choosing any new investment and talk to people smarter than I am.

To toot my own horn, these behaviors, according to research, tend to pay off in the long run. Dollar cost averaging works, buying indexes work, and long term holding works. Not for everyone, but for most people.

I’ll leave you with this question: What kind of investor are you? And how can you work with what you already have?

Other rants and reads

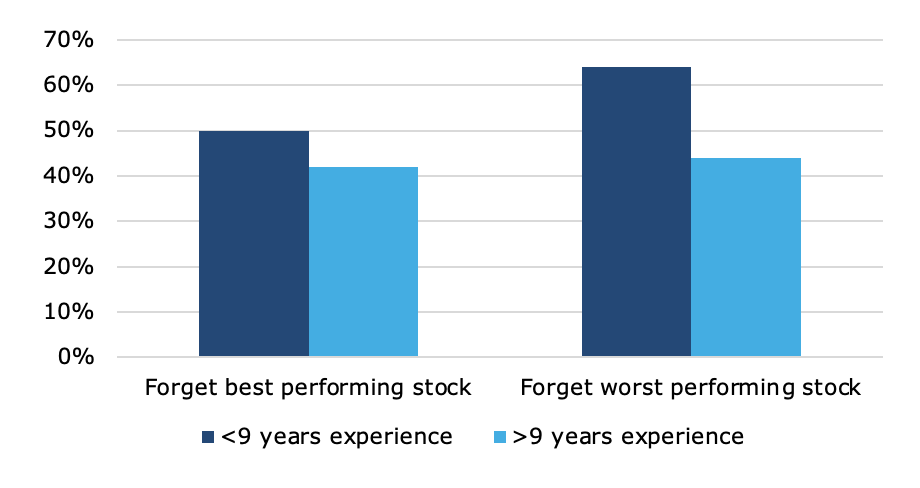

😶🌫️ Investors remember good picks and forget their worst ones

A recent study showed that most investors forget their worst stock picks and remember their best performers. Selective memory for the win!

The bright side: more experienced investors have better recall across the board.

If you want to remember your investing successes and wins, the easiest way is to journal about your investing. This is how I identified the type of investor I am (from today’s lead story).

My journaling is informal and not fancy. I just write down what happens every time I’m thinking through a big investment decision. It could be deciding to open up a crypto savings account or deciding to change the investments in my 401K.

Here’s a tip: you don’t need to track every trade. There are plenty of tools that automate that.

A better use of time is reflecting on investing behavior. Some example prompts:

- Why do you want to buy or sell an investment?

- Was there anything you wanted to invest in, but passed on? Why?

- What recent investment decisions do you celebrate or regret?

- How’s your current relationship with money? The stock market?

These prompts can apply more broadly to your financial life or included as part of an investing journal practice.

Reply: If you’re interested in more info or a template about this, respond with “Journal.” If I get 5 or more responses I’ll create a Notion template and share it with y’all in a future newsletter.

🏖 I must talk about Solana

When I attended UCSD, I’d sometimes take the Amtrak home to LA. The closest station was at Solana Beach. I remember cramming in and standing for 2 hours on busy rides.

Solana is a popular blockchain that borrows its name from San Diego roots: the founder Anatoly Yakovenko spent most of his career as a senior engineer at Qualcomm, also based in San Diego. Also, Solana also means sunshine (“sol”) and is often used as a Latin female name.

Solana is one of the many “Ethereum killers” that are competing in the same space: smart contracts, low fees and fast transactions. And it’s rapidly gaining legitimacy: Solana has done phenomenally well in terms of projects and price appreciation in the last few months. It’s now the 7th largest cryptocurrency by marketshare.

Here are a few starting points to learn about Solana:

- Interview with Solana Founder Anatoly Yakovenko — Acquired Podcast

- Everything you need to know about Solana — Bankless Podcast

- Solana Summer by Packy McCormick

- I’m taking Nat Eliason’s DeFi Course, and he suggests starting with Solana for experimenting with DeFi

Personally, I have invested a little bit (less than $1000) into Solana, but I’ve recently started a $100/week buy into the asset. I used Coinbase Pro for the initial buy and Voyager for the recurring.

P.S. let it be known that none of my content is investment, legal or financial advice. All are just opinions and I’m just a random dude on the internet.

🏔 ELI5: Evergrande Story

I’ve been seeing nothing by Evergrande headlines but didn’t dig into it til now. Here’s my “explain it like I’m 5” (ELI5) version of Evergrande, and implications as an investor.

- Evergrande is one of the biggest real estate developers in China (Wikipedia)

- To fuel aggressive growth, Evergrande took on tons of debt. It has $300 billion+ in liabilities, with about a third of that being in debt.

- The story first started breaking when Evergrande was not able to make back debt payments (defaulting)

- Evergrande’s stock continued sliding, and it’s causing ripple effects across China’s financial ecosystem

Why this matters to you and me: Evergrande is one of the biggest companies globally, and as such many funds—especially international ones—have exposure to China. When a company as big as Evergrande goes down, the impact is not just limited to the company – there can be a huge spillover effect to its partners and wider network.

Finance whiz Kyla Scanlon wrote about why Evergrande’s problem may not result in a Lehman Brother’s 2.0. She also points out that it may be a good idea to consider international funds that exclude China.

- The Freedom ETF (Ticker: FRDM) seeks to invest in countries with higher human and economic freedom scores.

- Emerging Markets Without China? – this article details which big funds have exposure to China, and various non-China funds to consider

As I’ve made abundantly clear, I’m not a trader. Especially not enough of one to come up with a momentum trade for this big story. From a long term portfolio perspective I’ll be a lot more wary of how much my overall portfolio is exposed to China.

⚖️ Lowest common denominator financial advice

Dave Ramsey will tell you to cut up credit cards. Suze Orman says you need at least $5 million to retire early. All financial gurus are pretty much saying the same thing: spend less, save more, avoid debt. *Yawn*

Then I realized the role these gurus play: dole out generic advice to the masses, resulting in what I call “lowest common denominator advice.” The advice is general, not specific.

This Forbes article puts it succinctly:

The financial advice you seek out depends on who you are. If you’re poor, you listen to Suze Orman. If you’re middle class, you listen to Dave Ramsey. But the rich think differently. They don’t take advice from Suze or Dave.

“Advice for you, not for me.”

Generalizations hide; specifics reveal: The more you dig into the specifics of how someone like Dave Ramsey is rich, you’ll start to realize it’s all about business building and using leverage. Not by cutting up credit cards or skipping lattes.

The advice he and other gurus give are more centered around not being poor versus becoming rich. There’s a value to this, since Americans are so deep in debt. But for those pursuing financial literacy, it’s important to identify the lowest common denominator financial advice and build up from there.

💸 Money Tip: Use Numbeo’s Cost of Living Calculator for Budgeting

Numbeo is a neat tool that shows cost of living around the world. Just enter your city and get a very detailed breakdown of all types of costs, from how much a family of 4 typically spend, to average costs for restaurants, groceries and even utilities.

Naturally, I looked up my hometown of Los Angeles and other favorites like Mexico City and Madrid.

This tool can be helpful for budgeting. People often wonder how much they should save. If you want to buy your freedom one month at a time, the estimated monthly costs can serve as a baseline.

Even more interesting is comparing the cost of living with other cities. Lots of people are moving now or excited about the prospect of being a digital nomad.

Seeing comparisons like this could really help ground financial part of moving to another city:

Just for fun:

Guy calls 911 high AF. “I looked down, and my hands were knives.”